Depreciation first becomes deductible when an asset is placed in service. The declining balance method uses the depreciation percentage amount each year rather than an equal amount. It is used as an accelerated depreciation method by companies wanting to reduce tax liability aggressively. Companies can select any depreciation method to allocate the cost of an asset proportionally. The monthly and yearly expense of depreciation is recorded on the income statement. The accumulated depreciation is recorded on the balance sheet of the company.

Best Accounting Software for Small Businesses of 2024

Common sense requires depreciation expense to be equal to total depreciation per year, without first dividing and then multiplying total depreciation per year by the same number. The table below illustrates the units-of-production depreciation schedule of the asset. There are several methods for calculating depreciation, generally based on either the passage of time or the level of activity (or use) of the asset. Note that ebitda definition while salvage value is not used in declining balance calculations, once an asset has been depreciated down to its salvage value, it cannot be further depreciated.

Businesses also use depreciation for tax purposes—namely, to reduce their total taxable income and, thus, reduce their tax liability. Under U.S. tax law, a business can take a deduction for the cost of an asset, thereby reducing their taxable income. But, in most cases, the cost of the asset must be spread out over time; this is called asset depreciation.

Units of Production Depreciation

As business accounts are usually prepared on an annual basis, it is common to calculate depreciation only once at the end of each financial year. The market value of the asset may increase or decrease during the useful life of the asset. However, the allocation of depreciation in each accounting period continues on the basis of the book value without regard to such temporary changes. All assets have a useful life and every machine eventually reaches a time when it must be decommissioned, irrespective of how effective the organization’s maintenance policy is. Depletion is another way in which the cost of business assets can be established in certain cases but it’s relevant only to the valuation of natural resources. The oil well’s setup costs can therefore be spread out over the predicted life of the well.

Also, it is seen as a business expense despite being a non-cash expense. Sum-of-years-digits is another accelerated depreciation method that gives greater annual depreciation in an asset’s early years. Fixed assets like buildings, vehicles, rental properties, commercial properties, and production equipment all decline over time. Depreciation is an accounting method used to calculate the decrease in value of a fixed asset while it’s used in a company’s revenue-generating operations.

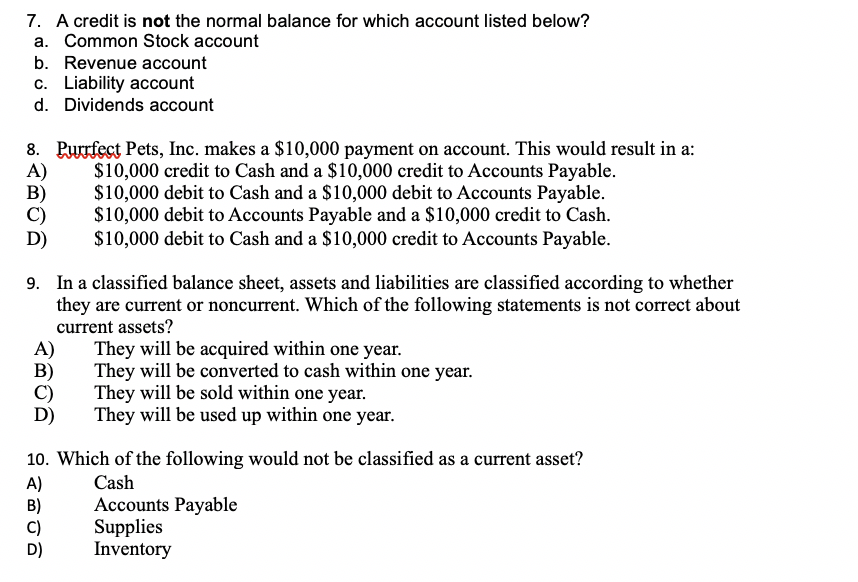

- The straight-line depreciation method gradually reduces the carrying balance of the fixed asset over its useful life.

- Tangible assets can often use the modified accelerated cost recovery system (MACRS).

- Businesses have some control over how they depreciate their assets over time.

- The Modified Accelerated Cost Recovery System, or MACRS, is another method for calculating accelerated depreciation.

Would you prefer to work with a financial professional remotely or in-person?

Here are four common methods of calculating annual depreciation expenses, along with when it’s best to use them. Depreciation is only applicable to physical, tangible assets that are subject to having their costs allocated over their useful lives. The cost of business assets can be expensed each year over the life of the asset to accurately reflect its use. The expense amounts can then be used as a tax deduction, reducing the tax liability of the business. The assumption behind accelerated depreciation is that the fixed asset drops more of its value in the earlier stages of its lifecycle, allowing for more deductions earlier on.

How to Build a Depreciation Schedule

Businesses depreciate long-term assets for both accounting and tax purposes. The decrease in value of the asset affects the balance sheet of a business or entity, and the method of depreciating the asset, accounting-wise, affects the net income, and thus the income statement that they report. Generally, the cost is allocated as depreciation expense among the periods in which the asset is expected to be used. Double declining balance depreciation is an accelerated depreciation method. Businesses use accelerated methods when dealing with assets that are more productive in their early years.

This may result in the asset being discarded even though it is still useful and in excellent physical condition. The application for automatic extension of time to file u s individual income tax return causes of depreciation include physical deterioration and obsolescence. The decisions that are made about how much depreciation to charge off are influenced by the accountant’s judgment.

Tangible assets may have some value when the business no longer has a use for them. Depreciation is therefore calculated by subtracting the asset’s salvage value or resale value from its original cost. The difference is depreciated evenly over the years of its expected life. The depreciated amount expensed each year is a tax deduction for the company until the useful life of the asset has expired. Some examples of fixed or tangible assets accounting bookkeeping for businesses that are commonly depreciated include buildings, equipment, office furniture, vehicles, and machinery. The formula to calculate the annual depreciation is the remaining book value of the fixed asset recorded on the balance sheet divided by the useful life assumption.